Our department moved offices in the last couple of weeks. As I was unpacking in my new digs (pictured below), something fell to the floor from box. Amazingly, after moves all over the world, I still have the first paper I wrote as a senior undergraduate in my Industrial Organization class 30 years ago – back when Sept. 11 was just another day at the beginning of the school year (cover photo).

I read it again, and as a Jutlander might say, ‘it’s not bad.’ What I knew at 20 about monopoly seems pretty true still today. I can see why I thought getting a PhD in economics might be fun and interesting.

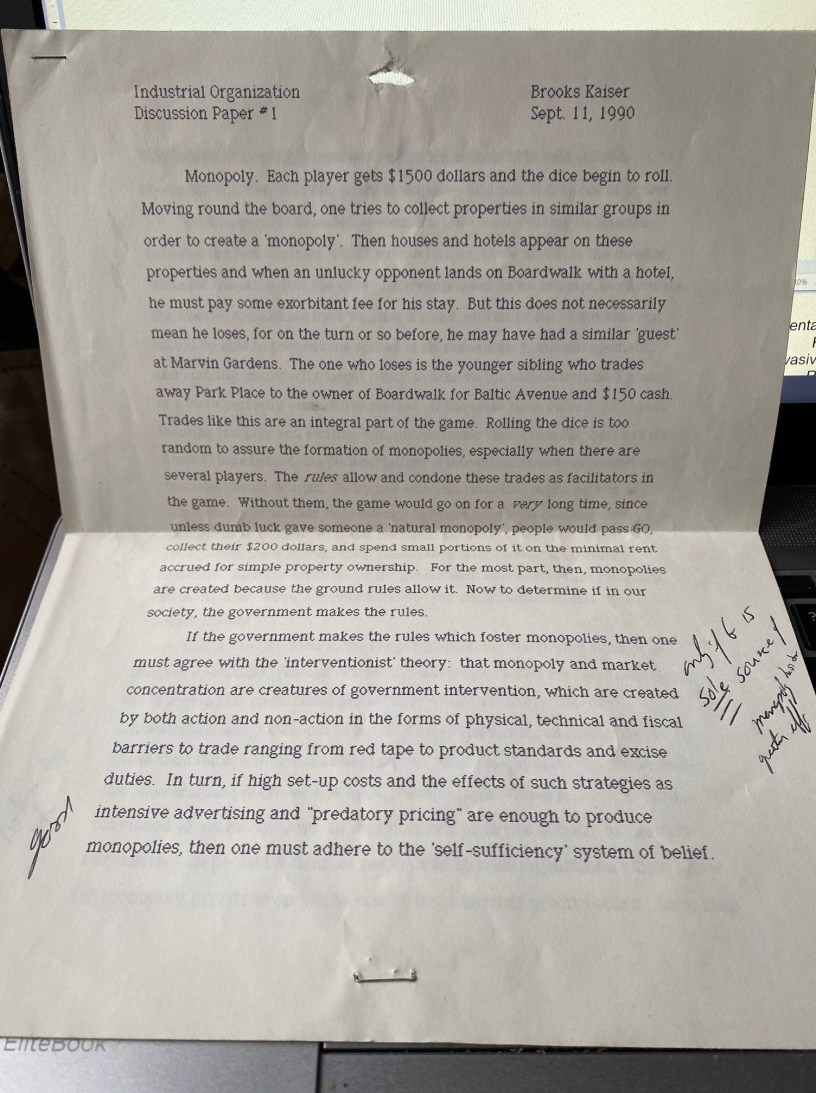

Here’s the text:

Industrial Organization Brooks Kaiser

Discussion Paper #1 Sept. 11, 1990

Monopoly. Each player gets $1500 dollars and the dice begin to roll. Moving round the board, one tries to collect properties in similar groups in order to create a ‘monopoly’. Then houses and hotels appear on these properties and when an unlucky opponent land on Boardwalk with a hotel, he must pay some exorbitant fee for his stay. But this does not necessarily mean he loses, for on the turn or so before, he may have had a similar ‘guest’ at Marvin Gardens. The one who loses is the younger sibling who trades away Park Place to the owner of Boardwalk for Baltic Avenue and $150 cash. Trades like this are an integral part of the game. Rolling the dice is too random to assure the formation of monopolies, especially when there are several players. The rules allow and condone these trades as facilitators in the game. Without them, the game would go on for a very long time, since unless dumb luck gave someone a ‘natural monopoly’, people would pass GO, collect their $200 dollars, and spend small portions of it on the minimal rent accrued for simple property ownership. For the most part, then, monopolies are created because the ground rules allow it. Now to determine if in our society, the government makes the rules.

If the government makes the rules which foster monopolies, then one must agree with the ‘interventionist’ theory: that monopoly and market concentration are creatures of government intervention, which are created by both action and non-action in the forms of physical, technical, and fiscal barriers to trade ranging from red tape to product standards and excise duties.[1] In turn, if high set up costs and the effects of such strategies as intensive advertising and “predatory pricing” are enough to produce monopolies, then one must adhere to the ‘self-sufficiency’ system of belief. This theory believes government regulation is desirable, and indeed necessary in order to break down monopolies and concentrations of power.

At this point it becomes obvious that the most striking difference between the two theories is that for the former, government is the disease, while for the latter it is the cure. Interventionists, in an attempt to eliminate the disease, are looking for a vaccine; a small, efficient dose of government should be able to prevent the spread of its bureaucracy, mismanagement, and inability to correctly target policy to achieve the self-determined goals of a more perfectly competitive market. If the same basic rules apply to all, insuring fair play and exciting competition rather than providing barriers for firms to hide behind, the positive factors of innovation and other competitive practices should flourish. To try and establish rules that might pertain to one industry or another, or to attempt to define where the demand curve lies when one is forced to define the consumer in such unrealistic ways (Who, for instance, is completely transitive in their choices?) is virtually impossible, and any ventures by the government into such realms generally end in disaster. Thus, interventionists would say government has done enough already.

But in the last decade, the Reagan decade, has the government done much of anything? The self-sufficiency advocates would say no. “Look at all the mergers that have taken place!” they would exclaim. “Market concentration has gotten out of hand. The government must stop this!” These calls for action seem at best naïve. Firms manipulate whatever they can. Government is one of the more flexible tools. [2] Government could be convinced to act many ways: to remain blind to firm’s actions, to provide bureaucracy to protect a firm, or perhaps to invoke regulations which allow for monopoly profits even while meant for a normal profit return. Each step becomes more and more entangled. No bureaucracy as large and unwieldy as the U.S. government is capable of making the wisest of choices among interests which by definition conflict. An overdose of medication tends to complicate the disease even further.[3]

John Bates Clark [sic] insight into the matter illustrates well the true dilemma.[4] He says, “In our worship of the survival of the fit under free natural selection we are sometimes in danger of forgetting that the conditions of the struggle fix the kind of fitness that come out of it;…and that only from strife with the right kind of rules can the right kind of fitness emerge (John B. Clark, The Control of Trusts [New York: Macmillan, 1912]pp.200-201).” The answer is not to intervene everywhere there seems to be trouble, with piecemeal regulation creating a bureaucracy of rules, loopholes, and entire fields for legal disputes, but rather to somehow create an environment in which such conflicting goals as productivity, efficiency,[5] innovation, the well-being of those involved on the production side of the industry, market stability in prices and supply, and reasonable prices to the consumers can all be reached to a greater extent. High levels of government intervention in such projects have proven disastrous, as with the European Community’s Common Agricultural Policy (CAP). But the lack of ‘guidelines’ has led to many abuses of power too, as the chapter in Adams is quick to point out. Perhaps it is best to say that monopoly does exist, the causes vary from bureaucracy to the absence of any rules, but that because it is difficult to pinpoint the actual diseased portions, government action does more to accentuate the problem than to arrest it. Until industry and production become gentlemen’s games, where it matters not whether one wins or loses, only how one plays, there will be no successful cure for these ills.

My thinking on these issues has become more resource oriented, as you can see with my 2018 chapter on Antitrust and Regulation in the Oxford Handbook of American Economic History, here. And I may now understand better the professor’s comment [1], even if I can’t actually decipher it. But it seems that more maybe now than ever (or at least, the last 120 years), the complex entanglements of government and market power could benefit from a very strong dose of decency. I wouldn’t use the term ‘gentlemen’s games’ to define fair dealing on a leveled playing field today, but I am definitely focused on working for some more and better cooperative behavior in 2021.

[1] Comment from professor: only if G is sole source of monopoly (indecipherable) greater eff.

[2] Comment from professor: interesting pt.

[3] Comment from professor: Are you saying that G intervention should actually be considered an aspect of the s-s [self sufficiency] theory? It’s plausible

[4] Comment from professor: Similar to Adams

[5] Comment from professor: what “rules” are ok – a la Adams “competitive market structure”??