In another post I have sung the praises of the late Martin Weitzman. Another economist who, by my own judgement, deserves as much respect is Sir Partha Dasgupta, who has quite recently written the magnificent: The economics of biodiversity: the Dasgupta review, for the UK Treasury. In a whopping 602 pages Dagupta explores the relation between biodiversity (or more broadly the environment) and the economy. His final conclusion is the title of this post.

In a way I am not the audience that Dagupta tried to reach with his review. In the preface of the review Dasgupta directly addresses finance, environment and health ministers in the 2nd paragraph. It’s these people and their employees, mainly the economists in those departments that the report is aimed at. However, although it does not shy away from mathematics, it is certainly not a mathematics-heavy academic article only aimed at economists. I am seriously considering it as a replacement for the book I currently use in my undergraduate course on environmental economics. It is, on the whole, very readable for the interested lay(wo)man.

Given its aim the content of the review is not very new or shocking to the average environmental/ resource economist. It is as Ben Groom and Zachary Turk call it: orthodox with an an unorthodox perspective at the centre. The focus is on the global or country level economy, and nature is an asset (also called natural capital), similar to manufactured capital and human capital. The price we pay for the use of natural capital is generally too low because there are externalities. We can use social cost-benefit analysis to judge the worth of marginal projects we undertake, but we will need valuation techniques to get closer to the true prices (also called accounting prices) that are to be used for such calculations. Gross Domestic Product is the wrong measure to keep track of our progress. None of this is particularly new or different for environmental / resource economists.

What is unorthodox is the way humanity and the economy are placed: not outside of nature, but embedded in it. This is the fault that Dasgupta refers to in the quote that is the title of this blog. By placing humanity and the economy embedded in nature we recognize that biodiversity’s values go beyond simple instrumental value, that there is also an existence value or perhaps even a moral worth.

Also, by placing the economy as embedded in nature we have to recognize that there is a carrying capacity, to use the biological term, a hard limit to the maximum size of the world economy, and perhaps even more important, this limit cannot be overcome by substitution of natural capital with other forms of capital or by human ingenuity. This is in stark contrast with most of the macroeconomic models that are used by your average macroeconomist, working in academia or at the government. It is also at odds with the integrated assessment models for climate change, such as those formulated by Nobel prize for economic sciences laureate William Nordhaus. In full fairness, it is not at all new to many ecological economists and a number of environmental economists, who have argued for hard limits to growth. Kenneth Boulding alludes to it in his Economics of the Coming Spaceship Earth, as does Weitzman in a comment to a paper by William Nordhaus, and even on this blog my colleague Villy Søgaard addresses the issue here and here.

That being said, let’s take a closer look at what is in the review. The review is very broad, and because there is also a shortened version and an overview of the key messages I will not summarize every chapter. Instead, I will pick up on the two main chapters, provide a few comments and take a few memorable quotes and messages.

The Review

I can only admire the careful job that has been done to get both the environmental and economic science side right. Dasgupta has worked with many ecologists (a.o. Simon Levin, Paul Ehrlich, Carl Folke and Marten Scheffer) and other environmental scientists, and this clearly shows in the level of understanding of natural processes and ecosystems and their inherent non-linearities and tipping points. Chapter 0, 2 and 3 are almost completely devoted to history, natural processes and ecosystems and how they are affected by disruptions, the complementarities and modularities that are part of ecosystems and how interventions in these can lead to different community structures, tipping points, hysteresis and irreversibilities. Furthermore, the causal relation between biodiversity and resilience is explored. After these chapters Dasgupta explores the economic side, although constantly referring back to these chapters, but he returns to the natural world in chapter 19 and 20 where we find ways to conserve and restore nature. For me personally, these chapters were like meeting old friends from my former field of study. I was also pleasantly surprised to see the Oostvaardersplassen feature rather prominently in the chapter on restoration, including the debate that lingers on in the Netherlands about the management or non-management of that area. I have written about the subject on this blog too.

The core of the review are chapters 4 and 13 (and their mathematical counterparts 4* and 13*). In chapter 4 Dasgupta introduces the impact inequality and an economic growth model where the economy is embedded in nature. The impact inequality is simply the expression that we currently use (demand) more of our natural resources than nature generates (supply), that is, we are mining our environment. Although this can be kept up for a long while because there are still stocks, at some point we will run out. Here Dasgupta does an admirable job bringing together some well-known metrics and models. For demand on the biosphere he uses a modified version of the well-known IPAT identity. Per unit human activity

Chapter 13 then introduces Dasgupta’s idea of how to measure and track sustainable development. People who know his work will not be surprised that this is through inclusive wealth. Inclusive wealth is the social worth of all capital, manufactured, human or natural. This value can be calculated by multiplying the amount of capital with its true price. Dasgupta then shows that if we want is to maximize intergenerational well-being, an increase in well-being is always accompanied by an increase in inclusive wealth. The objection that this framework implies complete substitutability between the different forms of capital is shown to be wrong: true prices in this framework depend on the stocks of all capital available. If little or no substitution is possible, the true price of the capital good in question would be (infinitely) high.

Some critical thoughts on the review and memorable excerpts

Critical thoughts

The review is an impressive piece of work, although most of it is not particularly new. The analysis of externalities in its most basic form goes back to at least to Pigou in the 1920’s, open access resources dates back to Gordon in 1954 or, according to my Danish colleagues, even to Jens Warming in 1911 and 1931.

Dasgupta also uses his own work on numerous occasions: the formal model for common property resources in chapter 8* is based on earlier work with Geoffrey Heal and on a chapter analysing institutions and common property resources, socially embedded preferences for the number of children in chapter 9 is a largely a repetition of his earlier work on this. And of course, inclusive wealth, including the well-being/wealth equivalence theorem has been shown by Dasgupta and Mäler and with others on numerous occasions.

The hard question, in my view, is how to exactly to track inclusive wealth. The problem is that it is very hard to track the physical amount of some of the forms of natural capital, let alone the true prices. The argument put forward by the review, however, is that it is better to keep track and get the prices roughly right, than to throw up our hands in despair and do nothing. The review in fairness does present a number of these estimates and also admits their inadequateness in terms of data availability and quality.

There is also another issue I see with inclusive wealth. Dasgupta is fairly critical of the alternatives that get formulated. He writes:

economic progress should be read as growth in inclusive wealth, not growth in GDP nor growth in any of the other ad hoc measures that have been proposed in recent years such as the UN’s Human Development Index.

The economics of biodiversity: the Dasgupta review, p. 121

and

The theorem implies that inclusive wealth is the right measure of intergenerational well-being, not GDP nor any of the other measures that have been suggested in recent years, such as the United Nations’ Human Development Index (HDI).

The economics of biodiversity: the Dasgupta review, p. 331

That may well be, but if we look at the underlying model is that Dasgupta uses for well-being it features a utility function

…the presumption that the sole factor in well-being is consumption may seem otiose. It is widely held instead that personal and social engagements are central to one’s sense of well-being; they shape the way one lives. But all engagements require goods and services; so, we may think of engagements as production activities, in which goods and services are inputs. Partaking of a meal (alone or in the company of others) is an engagement, but food items are the inputs that make the meal possible; friendship involves investment in time, which is a scarce resource; a walk in the countryside requires that there be a countryside; and so on.

The economics of biodiversity: the Dasgupta review, p. 283

So far, so good although one may still take issue with that argument. The utility then, however, gets added up over time (and discounted although there are good arguments for that too). That requires that utility is cardinal and can be added up between persons and generations. That in itself is not unheard of in welfare economics, but it is a fairly strong assumption. Many micro-economists do away with it, consider utility, if it exists, to be ordinal, and only use the utility function as a handy tool to describe behaviour about ranking preferences. A final problem I see with this, however, is that the correct true price for all forms of capital is to be expressed through its effect on well-being. That is determine the truly correct price we need:

- The effect of a change in any form of capital on any aspect of well-being

- An explicit function expressing well-being

both are extremely hard, if at all possible. So although inclusive wealth may be “the right measure of intergenerational well-being” it is only the right measure provided we have defined well-being correctly and when we’re willing to buy all the assumptions it rests on. Again, that does not make it a useless measure, far from it, but we should also not be blind to its limitations and the advantages of some of the other measures that have been proposed.

The one other thing I dislike about the review is that, in my mind, some thoughts are not continued or further explored. This may in part be space constraints (as mentioned the review is already 600 pages) or simply unknown material, but it leaves me as a reader dissatisfied.

For example in chapter 4*.2 Dasgupta formulates a model of economic growth including the impact inequality and a tipping point, but then leaves it at that. The model is not solved, there is no exploration of feasible growth paths, likely growth paths or sustainable growth paths (although the model is later used indirectly in the formulation of inclusive wealth). The model is only compared to existing models of economic growth and how they differ from the current one. Luckily, for me the earlier mentioned “review of the review” by Ben Groom and Zachary Turk does explore the model further.

Similarly chapter 10 of the review is an excellent chapter on the morality and reasons for discounting future well-being and consumption, and why we should discount future well-being and consumption at least at a modest rate. This chapter contains section 10.9 on dual discounting, the practice to discount projects that involve the environment at a lower rate than “normal”. Dasgupta writes about that practice:

Tempting though it is to conservationists, it would be unsafe to apply preferential discount rates even to nature-conservation projects, for there is always a risk the social evaluator will overlook to correct for capital gains and losses of some goods and services. The far safer practice would be to choose a numeraire, apply it to all projects, and measure benefits and costs on the basis of one set of accounting prices.

The economics of biodiversity: the Dasgupta review, p. 274

which leaves me with the question: all right fair enough, but what is to be our numeraire and how can we measure our accounting (true) prices in that numereaire?

Memorable excerpts

Total versus Marginal values

In the first chapter of the review Dasgupta introduces the notion of nature as an asset, including the true price we ought to pay for its use. If we talk about nature as an asset a famous paper comes to mind by Costanza et al. in which they estimated the total value of the world’s ecosystem services. Dasgupta points out the thinking flaw in that paper and manages to link it beautifully with the ethics in economics.

In a widely cited publication in Science, the authors estimated that the global flow of the biosphere’s services was, toward the end of the 20th century, worth US$16-54 trillion annually, with an average figure of US$33 trillion (Costanza et al. 1997). As that figure was larger than global Gross National Product (GNP) in the mid-1990s (estimated by the authors at the time to be approximately US$18 trillion annually) we were meant to appreciate the economic significance of the biosphere.

The economics of biodiversity: the Dasgupta review, p. 47

The estimate is a case of misplaced quantification. If the biosphere was to be destroyed, life would cease to exist. Who would then be here to receive US$33 trillion of annual benefits if humanity were to exchange its very existence for them? Economics, when used with care, is meant to serve our ethical values. The language it provides helps us to choose in accordance with those values. But the authors of the paper sought to persuade us that the biosphere is valuable because it can be imputed a large monetary value. That is to get things backward

On discounting

As already pointed out chapter 10 on discounting is excellent. It shows among others that discount rates are to be used carefully, and not, as is often done, treated as a simple constant parameter.

That CDRs are not independent of the reference stream is not a trivial observation. In a Focus article in The Economist (26 June 1999: 128), the author uncovered a disturbing tendency of compound interest to make large figures in the distant future look very small today:

“Suppose a long-term discount rate of 7 percent (after inflation) is used … Suppose also that … benefits (from a project) arrive 200 years from now … If global GDP grows by 3 percent a year during those two centuries, the value of the world’s output in 2200 will be US$8 quadrillion (a 16-figure number). But in present-value terms, that stupendous sum would be worth just US$10 billion. In other words, it would not make sense for the world to spend any more than US$10 billion (under US$2 a person) today on a measure that would prevent the loss of the planet’s entire output 200 years from now.”The argument is of course pure rubbish. Humanity would cease to exist if world output was to be zero. Where the author gets things wrong, after posing the problem, is to assume that the rates to be used for discounting future income losses are independent of the economic forecast that says there will be income losses. The final sentence in the passage points to the Ultimate Perturbation (zero world output in year 2200). The perturbation would involve a sharp decline in output just around year 2200. CDRs would be hugely negative in that brief period. So, where does the 7%-a-year discount rate come from? Discounting future incomes or consumption produces paradoxes only when it is not recognised that, as discount rates are features of the reference consumption stream around which investment projects are defined, they cannot be plucked from thin air.

The economics of biodiversity: the Dasgupta review, p. 274

The cruel choice we may be facing

In chapter 4 Dasgupta describes the impact inequality and puts it to use to arrive at some fairly stark and dark conclusions. One of those is about income inequality and the impact inequality

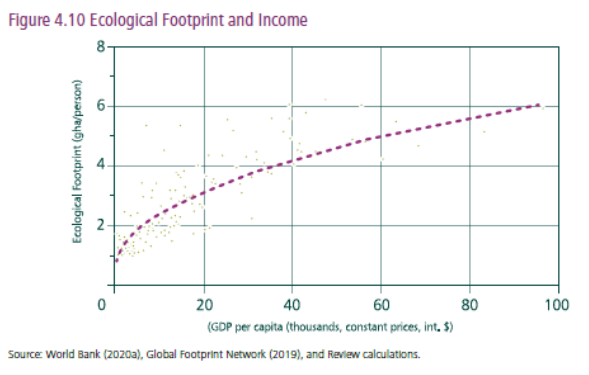

Figure 4.10, which displays a regression between the ecological footprint of nations and GDP per capita, shows that our demand for the biosphere’s goods and services increases with affluence and development but that the efficiency with which we transform them so increases with affluence that ecological footprint is a concave function

The economics of biodiversity: the Dasgupta review, p. 120

of income at all levels of incomes. In short, ecological footprint rises less than proportionately with income. That suggests, ominously, that egalitarian redistributions of incomes lead to larger global ecological footprints, other things the same

Now of course this is only valid given the current level of technology (called

We have defined the global ecological footprint by Ny/α. The Global Footprint Network (GFN) in contrast defines it as the ratio of the global demand for the biosphere’s goods and services and the biosphere’s current capacity to supply them on a sustainable basis (which we interpret here as G). The GFN’s global ecological footprint is then [Ny/α]/G. Wackernagel and Beyers (2019) report that the ratio increased from 1 in 1970 to 1.7 in 2019. That means the ratio increased at an average annual rate of 1.1%. Moreover, global GDP at constant prices has increased since 1970 at an average annual rate of 3.4%.

We turn to the right-hand side of the Impact Inequality. As noted previously, Managi and Kumar (2018) estimated that the value of per capita global natural capital declined by 40% between 1992 and 2014. That converts to an annual percentage rate of decline of 2.3%. But world population grew approximately at 1.1% in that period. Taken together it follows that the value of global natural capital declined at an annual rate of 1.2%. Because there are no estimates of the form of the G-function, we assume for simplicity that local variation is a good approximation, meaning that G is proportional to S. So, G can also be taken to have declined at an annual rate of 1.2%.

The estimates for the annual percentage rates of change of Ny, G, and [Ny/α]/G enable us to calculate that α had been increasing at an annual percentage rate of 3.5% in the period 1992 to 2014. Suppose we want to reach Impact Equality in year 2030. That would require [Ny/α]/G to shrink from its current value of 1.7 to 1 in 10 years’ time, implying that it must decline at an average annual rate of 5.4%. Assuming global GDP continues to grow at 3.4% annually and G continues to decline at 1.2% (i.e. business is assumed to continue as usual), how fast must α rise?

To calculate that, let us write as g(X) the percentage rate of change of any variable X. We then have

g([Ny/α]/G) = g(Ny) – g(α) – g(G) (B4.4.1)

Equation (B4.4.1) can be re-arranged as

g(α) = g(Ny) – g([Ny/α]/G) – g(G) (B4.4.2)

We now place the estimates of the terms on the right-hand side of equation (B4.4.2) to obtain

g(α) = 0.034 + 0.054 + 0.012 = 0.1In short, α must increase at an annual rate of 10.0%.

The economics of biodiversity: the Dasgupta review, p. 122-123

Dasgupta goes on to show that even if we took Draconian measures, freeze GDP growth and limit our detoriation of natural capital to 0.1% per year technological efficiency would still have to grow at 5.4% per year, which is really large compared to historical scenarios. So given current technological progress the SDGs themselves are unsustainable

What is to be done?

The review itself admits that given its global message it is hard to give very specific policy recommendations. It does explain that fixing this problem will require more than a few quick nuts and bolts, or as Dasgupta puts it “The choices are hard, they involve a lot more than a tax here and a set of regulations there.” (p. 33)

The review basically makes a few very general recommendations:

- Transform institutions and systems

- Empower citizens to make informed choices and implement change

- Create a global financial system that supports nature

- Adopt inclusive wealth

One last recommendation that is also made and that lies very close to my heart is to Reform education and economics to reflect the role of nature. Two last quotes on this then, the first especially directed at all curriculum designers and university boards:

There is every reason universities should require new students to attend a course on basic ecology. Field studies that would accompany such a course would be a way to connect students with Nature, in particular those who may have grown up in an urban environment. Understanding even the simplest of the biosphere’s processes may well be the first step toward developing a love of Nature

The economics of biodiversity: the Dasgupta review, p. 496

And the second as a reminder to myself and other parents:

Every child in every country is owed the teaching of natural history, to be introduced to the awe and wonder of the natural world, and to appreciate how it contributes to our lives.

The economics of biodiversity: the Dasgupta review, p. 496